Executive Summary

The Indian equity market has delivered exceptional returns post-2020, supported by abundant liquidity, policy reforms, and a surge in retail participation. However, as valuations stretch beyond historical norms and corporate earnings begin to plateau, the narrative of endless growth demands scrutiny. The question is no longer whether India is a growth story — are we still in a growth cycle, or has optimism crossed into speculative territory?

Understanding Market Valuations

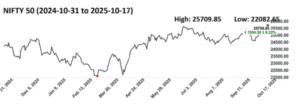

Over the past four years, benchmark indices have surged to record levels. The Nifty 50 currently trades near 22–23× earnings and 3.5× book value, while mid- and small-cap indices exceed 30× P/E, levels typically associated with exuberant sentiment rather than earnings visibility.

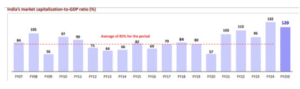

The Market Capitalization-to-GDP ratio, a broad measure of market froth, stands around 130-120%, surpassing its decade-long average of 87%. This suggests that market capitalization has grown faster than nominal GDP — a signal often observed in late- stage bull markets.

However, it’s essential to differentiate between systemic overvaluation and sector-specific excesses. Large-cap valuations remain anchored to reasonable growth assumptions, while froth is more concentrated in select themes — defence, infrastructure, and small-cap manufacturing.

Earnings vs. Price

Price momentum has far outpaced earnings momentum. Since 2020, the Nifty’s price has more than doubled, while aggregate earnings growth has moderated to single digits in FY25. Many large-cap Nifty 50 companies have delivered only 6% returns and key sectors such as private banking and IT are recording sub-10% PAT or revenue growth. Several heavyweights in IT, banking, and consumer sectors have missed earnings expectations, while midcap valuations remain disconnected from their profit trajectories.

This divergence highlights a classic late-cycle pattern, where market price stay inflated even as fundamentals normalise.

Unless earnings accelerate meaningfully in FY26, sustaining current multiples will be challenging.

Liquidity Effect

Post-2020, the flood of global liquidity, ultra-low interest rates, and accommodative RBI policy created fertile ground for price multiple expansion. As interest rates normalized (repo rate at 6.5%), the liquidity narrative shifted.

SIP as a percentage of total inflows … compare it with USA

SIPs now contribute close to ₹30,000 crore monthly, making retail investors the new backbone of India’s equity markets. It will be polarizing to assume that Retail Investors through SIPs are funding the super cycle. Such huge participation makes retail investors volnerable to market volatility.

The “Modi Effect”

Since Narendra Modi assumed office in 2014 and the Bharatiya Janata Party (BJP) formed a stable coalition government with over 240 seats, investor confidence in India’s growth story has soared. India’s trailing P/E ratio has frequently surpassed many other major economies: for example, India’s P/E stood around ~21.5× as of March 2025.

Given this backdrop, it would not be incorrect to say that Indian equities are priced not just on current fundamentals but on continuity of stable governance and policy momentum. If the political environment were disrupted, for example by the upcoming Bihar elections or subsequent state/central elections then market sentiment may face a significant stress-test. A disruption to the perceived policy stability could trigger heightened volatility in an environment where valuations already reflect optimism.

Government Stimulus

The government has not publicly conceded a slowdown, yet numerous fiscal measures point to a conscious effort to sustain demand.

For instance:

Ahead of elections, tax relief moved roughly ₹25,000 crore into the hands of households, thus boosting disposable income and consumption.

Most recently, the newly implemented Goods and Services Tax (India) (GST) reforms are projected to inject approximately ₹2 lakh crore to ₹2.5 lakh crore into the economy by lowering tax burdens and simplifying slabs.

Beyond these headline numbers, the scale and frequency of interventions suggest a pre-emptive approach, the government is leaning into stimulus even in the absence of a full-blown crisis.

In our view, if official data continues to portray robust growth while large-cap companies in the Nifty 50 universe report muted earnings, then the alignment between real economy and corporate performance weakens. Put differently: everything may not be as well-oiled as the public narrative suggests.

We believe a correction of 5-15 % in the equity market would not be unexpected, potentially offering a tactical entry point. We also note that as the US market (led by major technology stocks) shows signs of stress — including short-selling activity by prominent hedge funds and downward moves in marquee stocks such as NVIDIA (-4 %) and SoftBank Group Japan (-10 %) global spill-overs could trigger the Indian market’s moment of vulnerability.

______________________________________________________________________________________________________

The overall Indian equity market (Nifty/Sensex) is richly valued but not in an outright, unsustainable bubble yet, due to fundamental economic strength and resilient domestic flows. However, there is clear overheating in specific pockets (especially in some small- and mid-cap stocks).

______________________________________________________________________________________________________

Your Strategy

Avoid thematic and sectoral investments – Concentrated exposure to trending themes often delivers short-lived performance and amplifies downside risk when sentiment reverses.

Stay cautious on popular and expensive stocks – Valuations already discount future growth; such positions offer limited upside and disproportionate volatility.

Refrain from speculative trading – Leveraged positions in futures and options rarely align with long-term wealth objectives and can erode capital swiftly.

Adhere to your asset allocation and investment policy – Diversification and rebalancing are proven safeguards against behavioural bias and market noise.

Focus on risk-adjusted returns – Pursuing the highest nominal return often leads to disproportionate exposure to volatility and drawdowns.