Executive Summary

Income Plus Arbitrage Funds have emerged as a compelling solution for HNIs seeking stability, low volatility, and superior post-tax returns. These hybrid Fund-of-Fund (FoF) schemes blend debt mutual funds with equity arbitrage strategies, qualifying for equity-style taxation if held for over two years. In a post-2023 tax regime where traditional debt funds lost indexation benefits, this category offers a smart middle ground between fixed income and equity exposure.

What Are Income Plus Arbitrage Funds?

These funds typically allocate:

50–65% to debt mutual fund schemes (corporate bonds, G-Secs, floaters)

35–50% to arbitrage mutual funds (hedged equity positions)

This structure allows:

- Predictable income from debt

- Market-neutral gains from arbitrage

- Equity-like taxation if equity exposure ≥35% and held >24 months They are classified as FoFs, meaning they invest in other mutual fund schemes rather than directly in securities.

They are classified as FoFs, meaning they invest in other mutual fund schemes rather than directly in securities.

Risk & Return Profile

• Volatility: Lower than equity hybrid funds due to high debt allocation

• Sharpe Ratio: ~0.80–1.20 (varies by scheme) • Beta: ~0.60–0.80, indicating low market sensitivity

• Standard Deviation: ~2.4% (HSBC FoF) vs ~5– 6% for equity hybrids

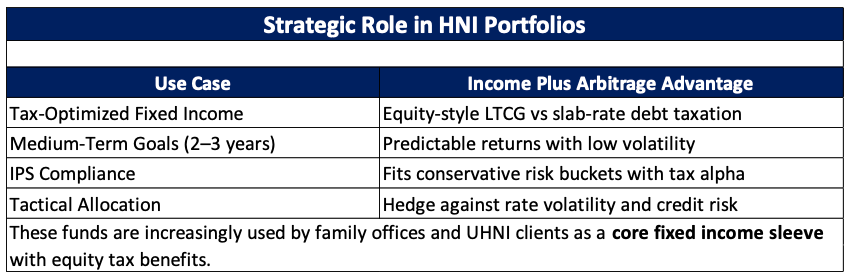

These funds are ideal for:

• Medium-term goals (2–3 years)

• Tax-sensitive investors

• Conservative portfolios seeking better-than- FD returns

Why Are These Funds Gaining Popularity?

Tax Efficiency: 60% lower tax outgo vs debt funds for HNIs

AUM Growth: ₹743 Cr (Apr 2023) → ₹3,161 Cr (Apr 2025)

No Tax on Internal Rebalancing: Debt-arbitrage switches happen at fund level

Dynamic Allocation: Managers adjust based on interest rates, arbitrage spreads

Diversification: Across asset classes and fund managers

Taxation (FY 2025–26)

Income Plus Arbitrage FoFs qualify for equity taxation if:

• ≥35% exposure to equity (via arbitrage funds)

• Held for >24 months Growth Option

STCG (<24 months): Taxed at investor’s slab rate (up to 30%)

LTCG (>24 months): Taxed at 12.5% + 4% cess Exemption: First ₹1.25 lakh LTCG per year is tax-free

NRI taxation: No TDS deductions subject to certain conditions.

Dividend Option

Taxed as per income slab.

TDS applicable if dividend >₹10,000/year

Operational Notes

Cut-off Time: Purchase before 3 PM for same-day

NAV

Redemption: Transaction +2 working days

Exit Load: Typically, 0.25% if redeemed within 30 days

Final Thoughts

In the current macro environment—marked by rate uncertainty, equity volatility, and evolving tax norms— arbitrage funds offer a low-risk, tax-efficient, and algorithmically managed solution for short-term capital deployment. For HNIs and corporate treasuries seeking stability without sacrificing returns, they remain a smart tactical choice.