Late into the night of 10–11 October 2025, the crypto world blinked and a friend’s entire leveraged portfolio vanished in hours. As someone who advises high-net- worth families and writes for a wealth-management audience, I believe that this incident is not just a cautionary anecdote but a deeply instructive case study in risk, discipline and humility.

My friend had positions in three marquee cryptocurrencies:

Bitcoin (BTC), Ethereum (ETH) and Solana (SOL).

All were 5×-leveraged trades on Binance.

Bitcoin: average entry $105,000 (USD). Stop-loss (limit) set at $122,000; liquidation at $108,000. Ethereum: average entry $4,150; stop-loss $3,822; liquidation at $3,500.

Solana similarly structured (though we focus here on BTC & ETH for clarity).

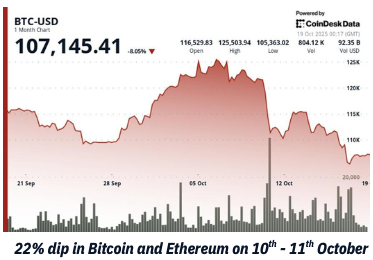

On 10–11 October, triggered in part by macro- geopolitical turbulence (notably the “trade war” rhetoric of Donald Trump and the resulting risk-off dynamics), the crypto market collapsed.

Bitcoin’s price plunged from a $122,000-plus range toward a low near ~$104,000 during the flash event. Ethereum fell from the ~$4,300-$4,400 region to lows around ~$3,435.

Order-books thinned. Liquidity evaporated. Over US$19 billion in leveraged crypto positions were liquidated in hours.

Because my friend used a stop-loss limit (SLL) rather than a stop-loss market (SLM), his trigger price never found a willing buyer at his limit during the rapid fall. The market simply dropped past his limit before the order could execute, so the liquidation event kicked in. The result: his entire position was wiped out.

From assured trader to zero-position in a matter of hours. He had sat on a large profit leg, telling himself “I will ride this further.”

But the market did not care about his conviction. The feeling of helplessness watching values collapse, knowing you had options but mis-executed them cannot be glossed over.

This isn’t a board-room mistake: it’s personal. It’s often internalised as “How could I be so stupid?” or “If only I had pressed the button earlier.”

My friend still continues to have shivers and he still thinks about that day.

For many who counsel families, we focus on strategy, tools, diversification. But the silent narrative of regret, the internal replay of “should-have/didn’t” is under- addressed. Under the glitz of crypto gains lies real, painful self-reproach when things go wrong.

Key Points to Remember

1. Understand Difference between SLL & SLM

A stop-loss limit (SLL) means you set a trigger price *and* a limit price. If the market moves too fast and skips past the limit, your order may never fill.

A stop-loss market (SLM) means when the trigger hits, your position submits a market order fills immediately at the best available price, albeit perhaps unfavourable.

My friend thought:

I’ll avoid being filled at the worst price → chose SLL → got completely skipped.

The lesson: In fast-moving, thin-liquidity markets (leveraged crypto is a prime example), SLM is often the safer option if the goal is *execution* rather than *optimising fill price*.

2. Liquidity Trigger

Any event that suddenly increases or drains the amount of money flowing into crypto markets.

When liquidity enters, prices jump faster. When it disappears, markets fall sharply — especially because crypto trades in thin, high-volatility environments.

3. Never deploy 100% of your powder

My friend used full commitment: every bit of margin, full leverage. No spare bullets. When the unexpected happens, you want optionality, breathing room, not fully committed.

In wealth-management terms: even in “high‐conviction” ideas, keep a buffer. Assume something can go wrong. Treat “cash on the sidelines” not as laziness but as insurance.

4. Adequate Capital Management + Greed vs Fear

He had a large profit leg. He could have taken some off, locked in profits, trimmed exposure.

He didn’t. Why?

Greed. “This will keep going.”

Meanwhile, fear of missing out dominated.

The saying from the popular trader, speaker and author Mark Douglas (author of The Disciplined Trader and Trading in the Zone) resonates:

“Anything can happen.”

He emphasises preparation for the unexpected, and the mindset of “I may be wrong” rather than “I am right.” My friend didn’t prepare. He believed continuation over possibility of rupture.

4. Do not invest money earmarked for other goals. Do not treat investing like a casino.

In his case: high-leverage bets, large chunk of capital, “all-in” mindset. This is speculation, not strategy.

For individuals – particularly those with multiple family goals, generational wealth concerns, legacy planning, the side of “investing” that looks like gambling is deadly.

Wealth management is about preservation, growth, risk- adjusted returns, optionality not “hit the grand slam” mindset each time.

Thankfully for my friend, all wasn’t lost permanently— there were other positions, diversification, and he’s still in business. But the emotional and reputational cost is real. He’s now far wiser (and measurably humbler).

Several clients of mine have told me:

“Okay, I know I want upside, but I also do not want what happened to him.”

For anyone reading be you high-net-worth, multi-family office client, family office advisor, wealth manager – this is not just a crypto anecdote.

The structures of risk apply across asset classes: leverage, liquidity risk, stop‐loss mechanics, behavioural biases.

The mindset of “This time is different” is perilous. The logic of “I’ll fix it later” or “I’ll ride it out” is dangerous when markets move fast.

Always ask: What happens if I’m dead wrong? And then build the plan, the buffer, the size-control accordingly.