SEBI on February 27, 2025, has introduced a new investment category called Specialized Investment Funds (SIF) to bridge the gap between traditional Mutual Funds (MFs) and Portfolio Management Services (PMS). This new framework, effective from April 1, 2025, offers investors more flexibility in their investment strategies while maintaining regulatory oversight. Let’s explore this new investment vehicle in detail.

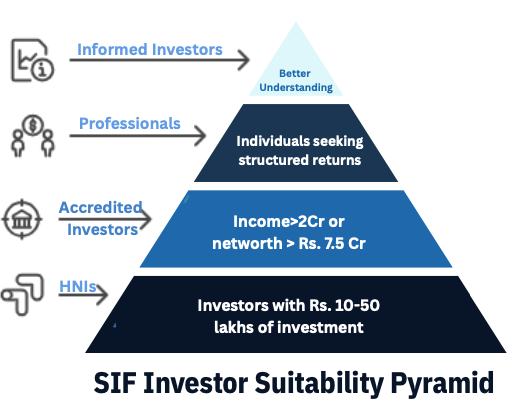

It is a distinct category which is aimed at sophisticated investors and High-Net-worth Individuals (HNIs). SIFs combine the pooled fund structure and regulatory oversight of mutual funds with the active, customized management approaches of high-ticket vehicles, addressing the demand for risk-managed, specialized investment solutions.

What is a Specialized Investment Fund?

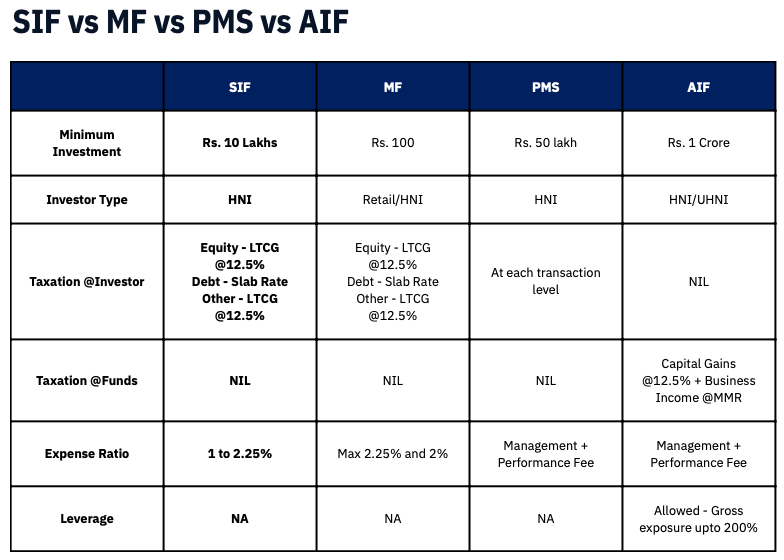

A Specialized Investment Fund is a new investment product regulated under the SEBI (Mutual Funds) Regulations, 1996. SIFs will offer greater portfolio flexibility than regular mutual funds while maintaining regulatory oversight. The framework will come into effect from April 1, 2025.

Key Features

1. Minimum

Rs. 10,00,000 across all the strategies.

2. Single, defined advanced strategy per scheme.

3. Combines mutual fund governance with AIF-style flexibility.

4. Interval or restricted redemption structures.

Who Can Launch SIFs?

Not every fund house can offer SIFs. SEBI has created two pathways for eligibility:

For established players: Mutual funds with 3+ years of operation and at least ₹10,000 crore average AUM in the last three years can launch SIFs, provided they have a clean regulatory record.

For newer entrants: Asset Management Companies (AMCs) can qualify by appointing specialized talent – including a Chief Investment Officer (CIO) with 10+ years of experience managing ₹5,000+ crore, and a Fund Manager with 3+ years of experience managing ₹500+ crore.

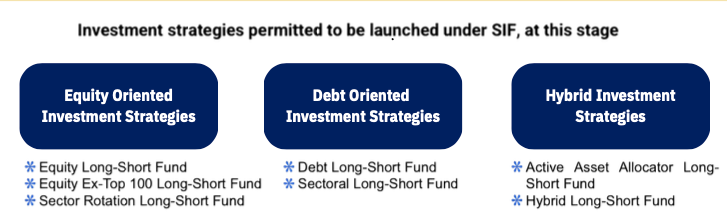

Equity Oriented Strategies –

Schemes: QSIF Equity Long-Short Fund

1. Equity Long Short Fund:

Min investment in equity & equity related instrument: 80%

2.Equity Ex-Top 100 Long Short Fund:

Min investment in equity & equity related instrument of stocks excluding top 100 stocks by market capitalization: 65%

3.Sector Rotation Long Short Fund

Min investment in equity & equity related instrument of max 4 sectors: 80%

For all the above strategies, Max short exposure through unhedged derivative positions in equity and equity related instruments: 25%

For Sector Rotation Long-Short Fund: Short exposure shall apply at the sector level, covering all stocks within that sector held in the portfolio. For instance, if the fund takes a short position in the Auto sector, all Auto sector stocks in the portfolio must be held as short positions

Debt Oriented Strategies –

Schemes: Arudha SIF (not yet public)

1. Debt Long Short Fund:

An interval debt investment strategy.

Investment in debt instruments across duration, including unhedged short exposure through exchange traded debt derivative instruments.

2.Sectoral Long Short Fund

Investment in debt instruments of at least two sectors, with max investment of 75% in a single sector

For all the above strategies, Max short exposure through unhedged derivative positions in debt related instruments: 25%

For Sectoral Long-Short Fund: Short exposure shall be across the sector, applicable for all the instruments of that particular sector held in the portfolio.

Hybrid Oriented Strategies –

Schemes: Altiva Hybrid Long-Short Fund, Magnum Hybrid Long-Short Fund

1. Active Asset Allocator Long-Short Fund :

An interval investment strategy dynamically investing across equity, debt, equity and debt derivatives, REITs/InVITs and commodity derivatives incl. limited short exposure

2.Hybrid LongShort Fund :

Interval investment strategy investing in

equity and debt securities.

Min investment in equity and equity related instruments: 25%

Min investment in debt instruments: 25%

For all the above strategies, Max short exposure through unhedged derivative positions in equity and debt related instruments: 25%

CEO Insights on Specialised Investment Funds (SIFs)

The core message revolves around moving beyond simplistic comparisons (like sorting by returns) and understanding SIFs as sophisticated, risk-managed solutions driven by their unique regulatory flexibility, particularly regarding derivative usage and tax efficiency.

1. Decoding Returns: The “Kitna Milega” Question

No Standard Answer: SIF returns are not homogenous, even within a single category, unlike traditional Mutual Funds (MFs).

. Nuanced Comparison is Key: An Equity Long-Short Fund with a 75% Long/25% Short structure will have a fundamentally different risk-return profile than a 25% Long/25% Short structure. Investors must compare funds based on their specific mandate and risk tolerance, not just by sorting on past returns.

2.The Core Flexibility and Purpose

Derivative Usage is the Key Differentiator: The fundamental flexibility of SIFs is the permission for derivative usage beyond simple hedging (which was the constraint in MFs).

Focus on Risk-Adjusted Returns: SIFs are primarily built to lower market exposure and risk while delivering a better risk-adjusted return, not just to chase higher absolute returns. Investors should evaluate SIFs through this lens.

No Leverage: Despite the use of derivatives, SIFs do not allow leverage as a structural feature; exposure is capped at 100%. Derivatives are simply financial tools that are valuable when used by capable managers, similar to how they are already used successfully in arbitrage funds.

3. Allocation Strategy: SIF as a “Solution,” Not an “Asset Class”

Don’t Allocate by Percentage: Investors should not ask, “How much should I allocate to SIF?”

Ask What it Solves: Instead, ask, “What financial solution does this SIF provide that I need?” For example, a Hybrid Long-Short SIF designed as a tax-efficient income solution is relevant for the debt or income component of a portfolio, but irrelevant if the portfolio only seeks aggressive growth assets.

4. Evaluation and Due Diligence

Tax Efficiency Matters: The greatest

advantage of SIFs is the structure, transparency, and tax efficiency of a Mutual Fund combined with alternative-like flexibility. Always compare the post-tax returns when benchmarking against PMS and AIFs.

SIFs

Data to Ask: To understand the potential investor experience, evaluate a SIF using data points like:

- Time Horizon

- Rolling Returns over 1-2 years

- Rolling Returns including Worst-Case Outcomes (1-month, 3-month)

- Standard Deviation (volatility measure)

- Open Market Exposure (Net exposure)

Manager Capability: SIFs require a different capability than simple buy-and-hold investing. Investors must question the AMC on their capability to manage sophisticated strategies, including different forms of shorting (fundamental, tactical, hedged derivatives).

Conclusion

SIF is a new asset class that is still evolving. Investors should prioritize understanding the product and its specific mandate before investing. Leveraging the expertise of good advisors and MFDs is essential for decoding these new funds.